Download our Link with Your Community Guide - A guide for finding meaningful and fun activities in your community and beyond.

Watch/Listen to our Podcast: Unstoppable Futures - Empowering Young Adults with Disabilities.

Download our Connecting The Dots Guide - A Guide to Finding Services for Children with Special Needs in Rhode Island.

-

Education

-

- Behavioral Health Services for Children and Youth

- BH Link

- Bradley Hospital Outpatient Services

- Community Care Alliance

- Community Mental Health Centers

- How to Connect with RI Certified Community Behavioral Health Clinics-CCBHC

- Mental Health Association of Rhode Island (MHARI)

- NAMI Rhode Island

- North American Family Institute (NAFI)

- Parent Support Network of Rhode Island (PSNRI)

- SUCCESS

- The Providence Center

- Thrive Behavioral Health Youth and Family Services

- Thrive Healthy Transitions

- Tides Family Services

-

- Back to School Cyber Safety

- Bullying and Youth with Disabilities

- Bullying-What You Can Do

- Cyberbullying

- Legislation Information

- Military Connected Youth and Bullying

- National Bullying Prevention Center-Students with Disabilities

- RI Bullying Guidance

- RI Department of Education - Bullying

- RI Statewide Bullying Policy

- RIPIN Tip Sheet - Addressing Bullying

- Supporting Students involved in Bullying

- What Can Schools Do About Bullying?

-

- Autism

- Blind and Visually Impaired

- Deaf or Hard of Hearing

- Developmental Disability

- Disability Resources (Rhode Island)

- Down Syndrome

- Driving - Adaptive Driving School Resource

- Emotional Disturbance Fact Sheet

- Intellectual Disability

- Learning Disability

- Other Health Impaired

- RIPIN Tip Sheet - IDEA Category: Emotional Disturbance

- RIPIN Tip Sheet - IDEA Disability Category : Autism

- RIPIN Tip Sheet - IDEA Disability Category Deaf-Blindness

- RIPIN Tip Sheet - IDEA Disability Category: Deafness

- RIPIN Tip Sheet - IDEA Disability Category: Hearing Impairment

- RIPIN Tip Sheet - IDEA Disability Category: Intellectual Disability

- RIPIN Tip Sheet - IDEA Disability Category: Multiple Disabilities

- RIPIN Tip Sheet - IDEA Disability Category: Orthopedic Impairment

- RIPIN Tip Sheet - IDEA Disability Category: Other Health Impairment

- RIPIN Tip Sheet - IDEA Disability Category: Specific Learning Disability

- RIPIN Tip Sheet - IDEA Disability Category: Speech or Language Impairment

- RIPIN Tip Sheet - IDEA Disability Category: Traumatic Brain Injury

- RIPIN Tip Sheet - IDEA Disability Category: Visual Impairment

- RIPIN Tip Sheet - IEP Eligibility in Rhode Island

- RIPIN Tip Sheet- IDEA Disability Category: Developmental Delay

- Special Needs Emergency Registry

- Traumatic Brain Injury

- Understanding the Professionals Supporting Your Child

- Show all articles ( 14 ) Collapse Articles

-

- Disciplina escolar y los derechos de los niños con un IEP o plan 504

- Manifestation Determination

- PBIS: What is the Family’s Role?

- Physical Restraint

- Physical Restraint - RI Regulations

- Q&A: IDEA Discipline Policy (Children with Disabilities)

- Restraint and Seclusion of Students with Disabilities

- Rhode Island Legal Services- Suspended from School?

- School Removal Procedures

- School Removals

- Understanding the rights of students with disabilities when it comes to discipline

- What is PBIS?

-

- "Stay Put" Rights: What They Are and How They Work

- CADRE Due Process Complaint Guide

- CADRE Due Process Resolution Session Guide

- CADRE IEP Facilitation Companion Video

- CADRE IEP Facilitation Guide

- CADRE Mediation Guide

- CADRE Written State Complaints Guide

- Dispute Resolution in Special Education

- Due Process Procedures

- Engaging Parents in Productive Partnerships

- Facilitated IEP/504 Meetings

- Preparing for a Facilitated IEP Meeting

- RI Data - Dispute Resolution

- RIDE - When Schools and Families Disagree

- RIDE Dispute Resolution Process

- RIPIN Tip Sheet - Collaborative Language for Schools and Parents

- RIPIN Tip Sheet - Prior Written Notice

- RIPIN Tip Sheet- How Should I Prepare For My Upcoming Meeting?

- Special Education Complaint Model Form

- Special Education Complaint Procedure

- VIDEO - Special Education Written State Complaints

- VIDEO: Preparing for Mediation

- VIDEO: Special Education Due Process

- VIDEO: Special Education Mediation

- VIDEO: Special Education Resolution Meetings

- Show all articles ( 10 ) Collapse Articles

-

- Bookshare Makes Reading Easier

- Dyslexia Resources

- How is Dyslexia Diagnosed?

- How to Support Your Child with Dyslexia

- IDENTIFICAÇÃO DA DISLEXIA

- Identifying Dyslexia

- Personal Literacy Plans

- Reading Tips for Families

- RIDE Literacy Learning Laboratory

- Right to Read - RI Regulations

- RIPIN Tip Sheet-The Difference between IEPs and 504 Plans

- Student Language and Literacy Profile

- The Rhode Island Right to Read Act - FAQ

- Tutoring - Reading and Dyslexia

- Understanding Dysgraphia

- Understanding Your Child's Evaluation Process

- Video: Dyslexia and the Brain

- Video: Inside a dyslexia evaluation

- Video: What is Dyslexia

- What Causes Dyslexia?

- What is Dyslexia?

- Writing Resources and Dyslexia

- Your Child's Special Education Eligibility Meeting

- Show all articles ( 8 ) Collapse Articles

-

- A Family’s Guide to Using AI for Advocacy In Early Intervention

- Applied Behavior Analysis (ABA) Therapy Fact Sheet

- BrightStars RI - Early Care and Education

- Cedar Family Center

- Child Outreach

- Early Childhood Resource Guide Ages 3-5

- Early Intervention Commonly Used Terms

- Early Intervention Fact Sheet

- Inclusion in Early Childhood Programs

- Katie Beckett

- Kids Connect Fact Sheet

- Respite Fact Sheet

- RI Early Intervention Procedural Safeguards

- RI Early Intervention Providers

- RI Early Learning & Development Standards

- RI Head Start Programs

- SUCCESS

- Understanding the Professionals Supporting Your Child

- Show all articles ( 3 ) Collapse Articles

-

- A Parent's Guide to Using AI for Advocacy In Special Education

- Communicating with Your Child's School-Steps to Success

- Drivers Education for Teens and Youth

- Family Educational Rights and Privacy Act (FERPA)

- GED (Rhode Island)

- Homeschooling - Frequently Asked Questions

- Individual Health Plans

- Informed School Choice: Questions to Ask When Considering Non-Public School Options for Your Child with Disabilities

- McKinney-Vento Act Quick Reference

- NCHE McKinney - Vento Eligibility Flowchart

- Parent Involvement

- Personal Literacy Plans

- RETENTION: Pros and Cons Chart

- RETENTION: What Parents Need to Know

- Rhode Island Legal Services- McKinney-Vento Act

- Rhode Island PTA Online Resource Guide

- RIDE-Students Experiencing Homelessness

- RIPIN Tip Sheet- How Should I Prepare For My Upcoming Meeting?

- RIPIN Tip Sheet- School Registration

- School Removals

- Translation - English to Spanish Glossary

- Truancy Court - Know Your Rights

- Tutoring

- Tutoring - K-12 Students

- Understanding the Professionals Supporting Your Child

- Show all articles ( 10 ) Collapse Articles

-

- Advocating for My Child’s Language and Disability Needs

- Bilingual Speech Therapy

- ELL - RIDE Regulations

- ELL Parent Resources

- Help Your Child Learn to Read

- Hoja de Consejos de RIPIN - ¿Cómo Puedo Traducir Sitios Web en mi Teléfono iPhone?

- Hoja de Consejos de RIPIN - ¿Cómo Puedo Traducir Sitios Web en mi Teléfono o Computadora (Google Chrome)?

- Hoja de Consejos de RIPIN - ¿Cómo Puedo Traducir Sitios Web en mi Teléfono o Computadora?

- MEETING THE NEEDS OF ENGLISH LEARNERS WITH AND WITHOUT DISABILITIES

-

- Dysgraphia Family & Tutor Toolkits

- Male Caregivers Guiding Teens with Disabilities Toward Adulthood

- MEETING THE NEEDS OF ENGLISH LEARNERS WITH AND WITHOUT DISABILITIES

- Military Family Readiness Academy

- Positive Behavioral Interventions and Supports (PBIS)- For Professionals

- Supporting Academic and Social Continuity for Mobile Elementary Students - OneOp

-

- RIPIN Tip Sheet - IDEA Category: Emotional Disturbance

- RIPIN Tip Sheet - IDEA Disability Category : Autism

- RIPIN Tip Sheet - IDEA Disability Category Deaf-Blindness

- RIPIN Tip Sheet - IDEA Disability Category: Deafness

- RIPIN Tip Sheet - IDEA Disability Category: Hearing Impairment

- RIPIN Tip Sheet - IDEA Disability Category: Intellectual Disability

- RIPIN Tip Sheet - IDEA Disability Category: Multiple Disabilities

- RIPIN Tip Sheet - IDEA Disability Category: Orthopedic Impairment

- RIPIN Tip Sheet - IDEA Disability Category: Other Health Impairment

- RIPIN Tip Sheet - IDEA Disability Category: Specific Learning Disability

- RIPIN Tip Sheet - IDEA Disability Category: Speech or Language Impairment

- RIPIN Tip Sheet - IDEA Disability Category: Traumatic Brain Injury

- RIPIN Tip Sheet - IDEA Disability Category: Visual Impairment

- RIPIN Tip Sheet - IEP Eligibility in Rhode Island

- RIPIN Tip Sheet- IDEA Disability Category: Developmental Delay

-

- Bringing Families to the Table

- Educator Strategies to Engage Families of Students with Intensive Needs

- How Can You Support Intensive Intervention? TIPS FOR FAMILIES

- Intensive Intervention - A Practitioner's Guide for Communicating with Parents and Families

- Intensive Intervention - An Overview for Parents and Families

- Intensive Intervention: Questions Parents and Families Can Ask

- Parent-Teacher Conferences: Strategies for Principals, Teachers and Parents

- WEBINAR - How to Use Family Engagement Educator Toolkit

-

- Civil Legal Resources

- Disability Rights Rhode Island (DRRI)

- Find an Education Lawyer

- Finding and Choosing a Lawyer

- Hoja de Consejos de RIPIN – Opciones de Toma de Decisiones para Adultos con Discapacidades

- Legal Support - RI Department of Education (RIDE)

- Pro Bono Volunteer Law Program

- Rhode Island Education Lawyers

- RI Legal Services

- RIPIN Tip Sheet - Decision-Making Options for Adults with Disabilities

- RIPIN Tip Sheet- Legal Resources

- Truancy Court - Know Your Rights

-

- Cyberbullying Safety Strategies for Kids and Teens

- EFMP- For Community Stakeholders

- Exceptional Family Member Program

- Exceptional Family Members Program (EFMP) Brochure

- Male Caregivers Guiding Teens with Disabilities Toward Adulthood

- Military Connected Youth and Bullying

- Military Family Readiness Academy

- Military One Source

- Military One Source (MOS) - Range of Support Card

- RI National Guard Family Assistance Center

- RIPIN Military Family Support Brochure

- Supporting Academic and Social Continuity for Mobile Elementary Students - OneOp

-

- Hoja de Consejos de RIPIN – Opciones de Toma de Decisiones para Adultos con Discapacidades

- RIPIN Tip Sheet - Addressing Bullying

- RIPIN Tip Sheet - Collaborative Language for Schools and Parents

- RIPIN Tip Sheet - Decision-Making Options for Adults with Disabilities

- RIPIN Tip Sheet - IEP Eligibility in Rhode Island

- RIPIN Tip Sheet - Least Restrictive Environment (LRE)

- RIPIN Tip Sheet - Prior Written Notice

- RIPIN Tip Sheet - The Special Education Referral Process

- RIPIN Tip Sheet- How Should I Prepare For My Upcoming Meeting?

- RIPIN Tip Sheet- Legal Resources

- RIPIN Tip Sheet- School Registration

- RIPIN Tip Sheet-The Difference between IEPs and 504 Plans

-

- Accommodations - ADA Testing

- Charter Schools and Section 504

- Disciplina escolar y los derechos de los niños con un IEP o plan 504

- Facilitated IEP/504 Meetings

- FAPE (Section 504)

- National Association of the Deaf-Section 504 and ADA Obligations of Public Schools

- Office of Civil Rights (OCR) - Parent and Educator Resource Guide

- Participating in Virtual Meetings

- Postsecondary Education, the ADA and Section 504

- Restraint and Seclusion of Students with Disabilities

- RIPIN Tip Sheet- How Should I Prepare For My Upcoming Meeting?

- RIPIN Tip Sheet-The Difference between IEPs and 504 Plans

- School Removals

- Section 504 - Hearing Procedures (RIDE)

- Section 504 of the Rehabilitation Act

- Understanding the Professionals Supporting Your Child

- Understanding the rights of students with disabilities when it comes to discipline

- What is a 504 plan?

- What is a 504 Plan?

- Show all articles ( 4 ) Collapse Articles

-

- A Guide to Disability Services -Rhode Island

- Advocates in Action

- Chart Your Own Future: How your Individualized Education Program can help

- Hoja de Consejos de RIPIN – ¿Cómo Debo Prepararme para mi Próxima Reunión?

- Legislative Self Advocacy

- Parent Guide to Help Students Prepare for Life and Work

- RIPIN Tip Sheet - Collaborative Language for Schools and Parents

- RIPIN Tip Sheet- How Should I Prepare For My Upcoming Meeting?

- Understanding Measurable Postsecondary Goals in the IEP

-

- BIP - What is a Behavior Intervention Plan?

- Discussing Behavioral Problems with Teachers

- Emotional Crisis Hotline - Kids' Link RI

- Emotional Support Via IEP or 504 Plan

- Getting Your Child Emotional Support at School

- Healthy Transitions Coping Cards

- Positive Behavioral Interventions and Supports (PBIS)- For Professionals

- RI Social Emotional Learning (SEL)

- School Refusal: When Kids Won't Do Schoolwork

- School Removals

- Social and Emotional Development in Early Childhood

- Social Emotional Learning: What You Need to Know

- SUCCESS

- Tantrums, Tears, and Tempers: How do I support my child’s mental health or challenging behaviors at home, in school, and in the community?

-

- (LRE) Least Restrictive Environment in Placement Decisions

- A Parent's Guide to Special Education

- A Parent's Guide to Using AI for Advocacy In Special Education

- Acronyms

- Basic Steps in Special Education

- Chart Your Own Future: How your Individualized Education Program can help

- Communicating with Your Child's School-Steps to Success

- Disciplina escolar y los derechos de los niños con un IEP o plan 504

- Extended School Year (ESY)

- Extended School Year (ESY) - What You Need to Know

- Facilitated IEP/504 Meetings

- Hoja de Consejos de RIPIN – ¿Cómo Debo Prepararme para mi Próxima Reunión?

- Hosting Virtual IEP Meeting Tip Sheets

- IEP Guidebook (Rhode Island IEP Form) - Age 3-13

- IEP Guidebook-Secondary

- IEP Overview

- IEP Parent Guide

- IEP Strength Based Fact Sheet

- IEP Tip Sheets

- Informed School Choice: Questions to Ask When Considering Non-Public School Options for Your Child with Disabilities

- Letter Writing Guide

- Manifestation Determination

- OSEP Glossary of Spanish Translations of Common IDEA Terms

- Participating in Virtual Meetings

- Procedural Safeguards

- RIDE - When Schools and Families Disagree

- RIPIN Tip Sheet - IEP Eligibility in Rhode Island

- RIPIN Tip Sheet - Least Restrictive Environment (LRE)

- RIPIN Tip Sheet - Prior Written Notice

- RIPIN Tip Sheet - The Special Education Referral Process

- RIPIN Tip Sheet- How Should I Prepare For My Upcoming Meeting?

- RIPIN Tip Sheet-The Difference between IEPs and 504 Plans

- School Removals

- Services beyond the school year for students with IEPs

- Special Education (RIDE)

- Special Education Complaint Model Form

- Special Education Complaint Procedure

- The IEP Process - FAQ and Flowchart

- Title 16 Education

- Understanding Measurable Postsecondary Goals in the IEP

- Understanding the Professionals Supporting Your Child

- Understanding the rights of students with disabilities when it comes to discipline

- Show all articles ( 27 ) Collapse Articles

-

- Cedar Family Center

- Department of Behavioral Healthcare, Development Disabilities & Hospitals (BHDDH)

- Developmental Disabilities (DD)

- Disability Rights Rhode Island (DRRI)

- Executive Office of Health and Human Service

- Office of Rehabilitation Services (ORS)

- Paul V. Sherlock Center on Disabilities at RIC

- Rhode Island Department of Education (RIDE)

- RI Coordinated Entry System (CES)/ Regional Access Points (RAPs)

- RI Department of Children, Youth & Families (DCYF)

- RI Developmental Disabilities Council

- RI Governors Commission on Disabilities

- Social Security Disability Benefits - Rhode Island

- Special Needs Emergency Registry

- SSI- How to apply?

-

- 5 myths about guardianship

- A Guide to Disability Services -Rhode Island

- BHDDH Adult Services Process – Students with DD

- BHDDH Application for DD Services

- BHDDH Brochure - What's Next for Me?

- Chart Your Own Future: How your Individualized Education Program can help

- Healthy Transitions Coping Cards

- LAW - RI Guardianship

- LAW - RI Supported Decision Making

- Parent Guide to Help Students Prepare for Life and Work

- Quality Assurance BHDDH Hotline - Suspected Abuse

- RIPIN Tip Sheet - Decision-Making Options for Adults with Disabilities

- SSI- How to apply?

- Supports Intensity Scale (SIS)

- Understanding Measurable Postsecondary Goals in the IEP

-

- Chart Your Own Future: How your Individualized Education Program can help

- Department of Behavioral Healthcare, Development Disabilities & Hospitals (BHDDH)

- Office of Rehabilitation Services (ORS)

- Parent Guide to Help Students Prepare for Life and Work

- Pre-Employment Transition Services-ORS

- Understanding Measurable Postsecondary Goals in the IEP

- YETI- What Youth Need to Know about Pre-Employment Services

-

- 5 myths about guardianship

- A Guide to Disability Services -Rhode Island

- Age of Majority / Transfer of Rights

- BHDDH - Behavioral Health Guide for Young Adults

- Chart Your Own Future: How your Individualized Education Program can help

- Dare to Dream Leadership Program

- DRRI Center for Supported Decision-Making (SDM)

- Employment- What Parents Can Do

- Healthy Transitions Coping Cards

- Link With Your Community Guide

- Mental Health in College-NAMI

- Navigation Checklist (for RI Individuals with Developmental Disabilities)

- Parent Guide to Help Students Prepare for Life and Work

- Person-Centered Planning

- Report Suspected Abuse Of Individuals With A Developmental Disability Or Individuals With A Disability Living In The Community

- Rhode Island Supported Decision-Making Guide

- RI Secondary Transition and Employment First

- RI Youth Transition Workbook

- RIPIN Tip Sheet - Decision-Making Options for Adults with Disabilities

- Social Security - Disability Benefits Application

- Social Security - Disability Facts

- Supplemental Security Income (SSI) for disabled adults and children

- Supported Decision Making (SDM) - Disability Rights RI

- Understanding Measurable Postsecondary Goals in the IEP

- YETI- What Youth Need to Know about Pre-Employment Services

- Show all articles ( 10 ) Collapse Articles

- (LRE) Least Restrictive Environment in Placement Decisions

- 5 myths about guardianship

- A Family’s Guide to Using AI for Advocacy In Early Intervention

- A Guide to Disability Services -Rhode Island

- A Parent's Guide to Special Education

- A Parent's Guide to Using AI for Advocacy In Special Education

- Advocating for My Child’s Language and Disability Needs

- Basic Steps in Special Education

- BH Link

- BIP - What is a Behavior Intervention Plan?

- Bookshare Makes Reading Easier

- Bradley Hospital Outpatient Services

- BrightStars RI - Early Care and Education

- Bringing Families to the Table

- CADRE Due Process Complaint Guide

- CADRE Due Process Resolution Session Guide

- CADRE IEP Facilitation Companion Video

- CADRE Mediation Guide

- CADRE Written State Complaints Guide

- Cedar Family Center

- Chart Your Own Future: How your Individualized Education Program can help

- Child Outreach

- Communicating with Your Child's School-Steps to Success

- Community Care Alliance

- Community Mental Health Centers

- Cyberbullying

- Cyberbullying Safety Strategies for Kids and Teens

- Derechos “Stay Put”: Qué son y cómo funcionan

- Disciplina escolar y los derechos de los niños con un IEP o plan 504

- Discussing Behavioral Problems with Teachers

- Dispute Resolution in Special Education

- Drivers Education for Teens and Youth

- Driving - Adaptive Driving School Resource

- Due Process Procedures

- Dysgraphia Family & Tutor Toolkit

- Dysgraphia Family & Tutor Toolkits

- Dyslexia Advocacy

- Dyslexia Resources

- Early Childhood Resource Guide Ages 3-5

- Educator Strategies to Engage Families of Students with Intensive Needs

- EFMP- For Community Stakeholders

- Emotional Crisis Hotline - Kids' Link RI

- Emotional Support Via IEP or 504 Plan

- Engaging Parents in Productive Partnerships

- Evaluating Children for Disability

- Exceptional Family Members Program (EFMP) Brochure

- Facilitated IEP/504 Meetings

- FBA - What is a Functional Behavioral Assessment?

- Frayer Model

- Free Recall Family & Tutor Toolkit

- Getting Your Child Emotional Support at School

- GreatSchools Test Guide for Parents - FAQ

- Growth Mindset for Parents

- Grupos de Apoyo Family Voices

- GUIDEBOOK: Advocacy in Action - A Guide to Local Special Education Parent Advisory Committees

- Healthy Transitions Coping Cards

- Help Your Child Learn to Read

- Hoja de Consejos de RIPIN - ¿Cómo Puedo Traducir Sitios Web en mi Teléfono iPhone?

- Hoja de Consejos de RIPIN - ¿Cómo Puedo Traducir Sitios Web en mi Teléfono o Computadora (Google Chrome)?

- Hoja de Consejos de RIPIN - ¿Cómo Puedo Traducir Sitios Web en mi Teléfono o Computadora?

- Hoja de Consejos de RIPIN – ¿Cómo Debo Prepararme para mi Próxima Reunión?

- How Can You Support Intensive Intervention? TIPS FOR FAMILIES

- How is Dyslexia Diagnosed?

- How to Support Your Child with Dyslexia

- IDENTIFICAÇÃO DA DISLEXIA

- Identifying Dyslexia

- IEP Guidebook (Rhode Island IEP Form) - Age 3-13

- IEP Guidebook-Secondary

- IEP Tip Sheets

- Inclusion in Early Childhood Programs

- Individual Health Plans

- Informed School Choice: Questions to Ask When Considering Non-Public School Options for Your Child with Disabilities

- Instructional Intervention: What You Need to Know

- Intensive Intervention - A Practitioner's Guide for Communicating with Parents and Families

- Intensive Intervention - An Overview for Parents and Families

- Intensive Intervention: Questions Parents and Families Can Ask

- Katie Beckett

- Male Caregivers Guiding Teens with Disabilities Toward Adulthood

- Manifestation Determination

- McKinney-Vento Act Quick Reference

- MEETING THE NEEDS OF ENGLISH LEARNERS WITH AND WITHOUT DISABILITIES

- Mental Health Association of Rhode Island (MHARI)

- Mental Health in College-NAMI

- Military Connected Youth and Bullying

- Military Family Readiness Academy

- Military One Source (MOS) - Range of Support Card

- NAMI Rhode Island

- National Association of the Deaf-Section 504 and ADA Obligations of Public Schools

- National Bullying Prevention Center-Students with Disabilities

- NCHE McKinney - Vento Eligibility Flowchart

- North American Family Institute (NAFI)

- Parent Guide to Help Students Prepare for Life and Work

- Parent Support Network of Rhode Island (PSNRI)

- Parent-Teacher Conferences: Strategies for Principals, Teachers and Parents

- PBIS: What is the Family’s Role?

- Person-Centered Planning

- Personal Literacy Plans

- Physical Restraint

- Physical Restraint - RI Regulations

- Positive Behavioral Interventions and Supports (PBIS)- For Professionals

- Postsecondary Education, the ADA and Section 504

- Pre-Employment Transition Services-ORS

- Q&A: IDEA Discipline Policy (Children with Disabilities)

- Quality Assurance BHDDH Hotline - Suspected Abuse

- Reading Tips for Families

- Rhode Island Legal Services- McKinney-Vento Act

- Rhode Island Legal Services- Suspended from School?

- Rhode Island PTA Online Resource Guide

- RI Data - Dispute Resolution

- RI Secondary Transition and Employment First

- RI Social Emotional Learning (SEL)

- RIDE - When Schools and Families Disagree

- RIDE Literacy Learning Laboratory

- RIDE-Students Experiencing Homelessness

- Right to Read - RI Regulations

- RIPIN Peer Groups

- RIPIN Tip Sheet - Addressing Bullying

- RIPIN Tip Sheet - Collaborative Language for Schools and Parents

- RIPIN Tip Sheet - Decision-Making Options for Adults with Disabilities

- RIPIN Tip Sheet - IDEA Category: Emotional Disturbance

- RIPIN Tip Sheet - IDEA Disability Category : Autism

- RIPIN Tip Sheet - IDEA Disability Category Deaf-Blindness

- RIPIN Tip Sheet - IDEA Disability Category: Deafness

- RIPIN Tip Sheet - IDEA Disability Category: Hearing Impairment

- RIPIN Tip Sheet - IDEA Disability Category: Intellectual Disability

- RIPIN Tip Sheet - IDEA Disability Category: Multiple Disabilities

- RIPIN Tip Sheet - IDEA Disability Category: Orthopedic Impairment

- RIPIN Tip Sheet - IDEA Disability Category: Other Health Impairment

- RIPIN Tip Sheet - IDEA Disability Category: Specific Learning Disability

- RIPIN Tip Sheet - IDEA Disability Category: Speech or Language Impairment

- RIPIN Tip Sheet - IDEA Disability Category: Traumatic Brain Injury

- RIPIN Tip Sheet - IDEA Disability Category: Visual Impairment

- RIPIN Tip Sheet - IEP Eligibility in Rhode Island

- RIPIN Tip Sheet - Least Restrictive Environment (LRE)

- RIPIN Tip Sheet - Prior Written Notice

- RIPIN Tip Sheet - The Special Education Referral Process

- RIPIN Tip Sheet- How Should I Prepare For My Upcoming Meeting?

- RIPIN Tip Sheet- IDEA Disability Category: Developmental Delay

- RIPIN Tip Sheet- Legal Resources

- RIPIN Tip Sheet- School Registration

- RIPIN Tip Sheet-The Difference between IEPs and 504 Plans

- School Removal Procedures

- School Removals

- SEAN Meeting Presentation - 11.7.19 (Technical Assistance Guidebook)

- Section 504 of the Rehabilitation Act

- Services beyond the school year for students with IEPs

- Servicios del año escolar extendido: Lo que necesita saber

- Social Emotional Learning Parent Toolkit

- Social Skills Groups - Groden Center

- SOCIAL STORY - How To Protect Yourself and Others

- Special Education Complaint Model Form

- Special Education Complaint Procedure

- Student Language and Literacy Profile

- SUCCESS

- Supporting Academic and Social Continuity for Mobile Elementary Students - OneOp

- Supporting Students involved in Bullying

- Tantrums, Tears, and Tempers: How do I support my child’s mental health or challenging behaviors at home, in school, and in the community?

- The Providence Center

- The Rhode Island Right to Read Act - FAQ

- Thrive Behavioral Health Youth and Family Services

- Thrive Healthy Transitions

- Tides Family Services

- Title 16 Education

- Translation - English to Spanish Glossary

- Traumatic Brain Injury

- Truancy Court - Know Your Rights

- Tutoring - Reading and Dyslexia

- Understanding Common Assessments (Video)

- Understanding Dysgraphia

- Understanding Measurable Postsecondary Goals in the IEP

- Understanding the Professionals Supporting Your Child

- Understanding the rights of students with disabilities when it comes to discipline

- Understanding Your Child's Evaluation Process

- Understanding Your Child's Trouble with Math

- Video: Dyslexia and the Brain

- Video: Inside a dyslexia evaluation

- VIDEO: MTSS - RI Family Guide

- VIDEO: STAR Screening Report - A Family Guide

- Video: What is Dyslexia

- WEBINAR - Special Education Local Advisory Committees

- What Causes Dyslexia?

- What is a 504 plan?

- What is Dyslexia?

- What is MTSS (Multi-Tiered System of Supports)?

- What is PBIS?

- What is RTI: Response to Intervention ?

- Why are Special Education Advisory Committees (SEAC) Needed?

- Writing Resources and Dyslexia

- YETI- What Youth Need to Know about Pre-Employment Services

- Your Child's Special Education Eligibility Meeting

- Show all articles ( 175 ) Collapse Articles

-

Family

-

- Family Voices Resource Guide (English)

- Family Voices RI Support Groups Guide 2019

- Guía de recursos de Family Voices

- Hoja de Consejos de RIPIN - ¿Cómo Puedo Traducir Sitios Web en mi Teléfono iPhone?

- Hoja de Consejos de RIPIN - ¿Cómo Puedo Traducir Sitios Web en mi Teléfono o Computadora (Google Chrome)?

- Hoja de Consejos de RIPIN - ¿Cómo Puedo Traducir Sitios Web en mi Teléfono o Computadora?

- Link With Your Community Guide

- RI Family Guide

-

Health

-

- Articles coming soon

-

Health Insurance

-

- Appeal Writing Guide - Medical Necessity

- APTC & CSR Eligibility - Income and Household Size

- APTC & CSR Eligibility – Access to Other Coverage

- Mental Health Parity

- QHP - Basic Eligibility Rules

- QHP - Billing, Grace Periods, and Termination

- QHP - Coverage & Benefits

- QHP - Key Documents & Contacts for Advocates

- QHP & MAGI Medicaid – How & When to Apply

- QHP & Medicaid Eligibility Appeals

- Reading Paystubs: Where's the MAGI?

-

- Articles coming soon

-

- Articles coming soon

-

Youth & Young Adults

-

- A Guide to Disability Services -Rhode Island

- Drivers Education for Teens and Youth

- Mental Health in College-NAMI

- RIPIN Tip Sheet- How Should I Prepare For My Upcoming Meeting?

- SAT/PSAT - When to Request Accommodations

- Supporting Transgender Youth In School

- Video: Dyslexia and the Brain

- Video: Inside a dyslexia evaluation

- Video: What is Dyslexia

- Writing Resources and Dyslexia

- YETI- What Youth Need to Know about Pre-Employment Services

-

- A Guide to Disability Services -Rhode Island

- Advocates in Action

- Dare to Dream Leadership Program

- Discrimination Protection - Office of Civil Rights

- DRRI Center for Supported Decision-Making (SDM)

- Hoja de Consejos de RIPIN – Opciones de Toma de Decisiones para Adultos con Discapacidades

- How To Build Resilience

- How to Vote and Your Rights

- IEP Meeting Checklist for Students

- PACER - Advocating from Myself

- PFLAG Greater Providence

- PODCAST: Unstoppable Futures

- RIPIN Tip Sheet - Decision-Making Options for Adults with Disabilities

- Sherlock Sentinels Advisory Committee

- Supported Decision Making (SDM) - Disability Rights RI

- The Trevor Project

- VIDEO - Supported Decision-Making

- WAZE to Adulthood - Planning for YOUR Future

- Youth Pride Inc.

- Show all articles ( 4 ) Collapse Articles

-

-

Recursos en Espanol

-

- Cartões de enfrentamento de transições saudáveis

- Escuela Elemental

- Escuela Intermedia y Superior

- Guía para padres sobre el uso de la IA (Inteligencia Artificial) para apoyar la defensa de sus hijos en la Intervención Temprana y Educación especial

- Hoja de Consejos de RIPIN – ¿Cómo Debo Prepararme para mi Próxima Reunión?

- Hoja de Consejos de RIPIN – Opciones de Toma de Decisiones para Adultos con Discapacidades

- IDENTIFICAR LA DISLEXIA

- Información de la disciplina escolar

- Los Derechos Educativos de la Familia y la Ley de Privacidad (FERPA)

- Participación de padres

- RIDE Literacy Learning Laboratory

- Tarjetas de afrontamiento para transiciones saludables

- Traducción - Glosario Español

-

- BIP - ¿Qué es un Plan de Intervención del Comportamiento?

- Cartões de enfrentamento de transições saudáveis

- Cómo Elegir una Escuela: Preguntas que debe hacer cuando considera opciones para escuelas no públicas para su hijo con discapacidades

- Comunicándose con la Escuela a Través de Cartas

- Comunicándose con la Escuela a Través de Cartas

- Consejos Claves Sobre EL Programa IEP Para Padres de Familia: Generalidades del IEP

- Consideración de LRE en las Decisiones de Colocación

- Considerando la Tecnología de Asistencia

- Derechos “Stay Put”: Qué son y cómo funcionan

- Desarrollando el IEP de Su Hijo

- Edades 14 al 21 años

- Edades 3 al 13 años

- Educacion Especial Guia Para Padres

- Esquema del PEI

- FBA - ¿Qué es una evaluación del comportamiento funcional?

- Formulario de modelo de queja de educación especial

- Garantías procesales

- Guía de padres del PEI (IEP)

- Guía para padres sobre el uso de la IA (Inteligencia Artificial) para apoyar la defensa de sus hijos en la Intervención Temprana y Educación especial

- Hoja de Consejos de RIPIN – ¿Cómo Debo Prepararme para mi Próxima Reunión?

- IDENTIFICAR LA DISLEXIA

- Mediación

- Procedimiento de la queja de educación especial

- Servicios del año escolar extendido: Lo que necesita saber

- Tarjetas de afrontamiento para transiciones saludables

- Un IEP Facilitado y las Juntas de Sección 504

- Show all articles ( 11 ) Collapse Articles

-

- Brightstars RI -Un programa de Aprendizaje Temprano

- Cedar Centro Familiar

- Garantias Procesales y Financiamiento de Intervención Temprana de Rhode Island

- Guía para padres sobre el uso de la IA (Inteligencia Artificial) para apoyar la defensa de sus hijos en la Intervención Temprana y Educación especial

- Head Start De Rhode Island

- Hoja Informativa de Kids Connect

- Hoja Informativa de Terapia de Análisis Conductual Aplicado

- Hoja Informativa del Programa de Intervención Temprana

- Hoja Informativa del Programa de Relevo

- Hoja Informativa del Programa Katie Beckett

- Inclusion en los Programas de Educacion Temprana

- Normas en RI de Desarrollo y Aprendizaje

- Proveedores de Intervencion Temprana

-

- Derechos legales en el proceso de evaluación: Lo que necesita saber

- Entender las evaluaciones

- Evaluación: ¿Qué significa para su hijo?

- Evaluaciones privadas versus evaluaciones en la escuela: ventajas y desventajas

- Evaluaciones privadas: Qué necesita saber

- IDENTIFICAR LA DISLEXIA

- La Evaluación Gratuita de Niños

- Pasos básicos en la educación especial

-

- Hoja de Consejos de RIPIN - ¿Cómo Puedo Traducir Sitios Web en mi Teléfono iPhone?

- Hoja de Consejos de RIPIN - ¿Cómo Puedo Traducir Sitios Web en mi Teléfono o Computadora (Google Chrome)?

- Hoja de Consejos de RIPIN - ¿Cómo Puedo Traducir Sitios Web en mi Teléfono o Computadora?

- Hoja de Consejos de RIPIN – ¿Cómo Debo Prepararme para mi Próxima Reunión?

- Hoja de Consejos de RIPIN – Opciones de Toma de Decisiones para Adultos con Discapacidades

-

- 5 Mitos Sobre la Tutela

- Cómo obtener un documento notarizado

- Como solicitar ayuda - DDRI (Seleccione el idioma español en la opción que se encuentra arriba a la derecha)

- Directivas Avanzadas-Poder Notarial

- Guía práctica para la toma de decisiones con apoyo de Rhode Island

- Hoja de Consejos de RIPIN – Opciones de Toma de Decisiones para Adultos con Discapacidades

- Planificación Futura: Donde Empezar

- ssa.gov/es-Como administrar sus beneficios-Seguro Social

-

- 5 Mitos Sobre la Tutela

- Departamento de Salud del Comportamiento, Discapacidades del Desarrollo y Hospitales (BHDDH)

- Hoja de Consejos de RIPIN – Opciones de Toma de Decisiones para Adultos con Discapacidades

- PROCESO DE SERVICIOS PARA ADULTOS DE BHDDH - División de Discapacidades del Desarrollo

- SOLICITUD BHDDH PARA SERVICIOS DD

- 5 Mitos Sobre la Tutela

- BIP - ¿Qué es un Plan de Intervención del Comportamiento?

- Cartões de enfrentamento de transições saudáveis

- Cómo Elegir una Escuela: Preguntas que debe hacer cuando considera opciones para escuelas no públicas para su hijo con discapacidades

- Comunicándose con la Escuela a Través de Cartas

- Consejos Claves Sobre EL Programa IEP Para Padres de Familia: Generalidades del IEP

- Defienda los derechos lingüísticos y de accesibilidad de su hijo/a

- Departamento de Salud del Comportamiento, Discapacidades del Desarrollo y Hospitales (BHDDH)

- Derechos legales en el proceso de evaluación: Lo que necesita saber

- Educacion Especial Guia Para Padres

- Entender las evaluaciones

- Evaluaciones privadas versus evaluaciones en la escuela: ventajas y desventajas

- Evaluaciones privadas: Qué necesita saber

- FBA - ¿Qué es una evaluación del comportamiento funcional?

- Grupos de Apoyo Family Voices

- Guía para padres sobre el uso de la IA (Inteligencia Artificial) para apoyar la defensa de sus hijos en la Intervención Temprana y Educación especial

- Hoja de Consejos de RIPIN - ¿Cómo Puedo Traducir Sitios Web en mi Teléfono iPhone?

- Hoja de Consejos de RIPIN - ¿Cómo Puedo Traducir Sitios Web en mi Teléfono o Computadora (Google Chrome)?

- Hoja de Consejos de RIPIN - ¿Cómo Puedo Traducir Sitios Web en mi Teléfono o Computadora?

- Hoja de Consejos de RIPIN – ¿Cómo Debo Prepararme para mi Próxima Reunión?

- Hoja de Consejos de RIPIN – Opciones de Toma de Decisiones para Adultos con Discapacidades

- IDENTIFICAR LA DISLEXIA

- Intervención Intensiva - Consejos Para Familias

- Intervención Intensiva - Consejos Para Familias

- Introducción y alcance del kit de herramientas

- Kits de recursos sobre disgrafia para familias y tutores

- La Evaluación Gratuita de Niños

- La intervención intensiva - Un resumen para padres y familias

- Modelo de prestación de servicios de Educación Especial Temprana Itinerante (IECSE) de Rhode Island

- RI Rental Resource Guide (Spanish) Guía de recursos de alquiler en Rhode Island

- RIDE Literacy Learning Laboratory

- Servicios de Transición Previos al Empleo-Oficina de Servicios de Rehabilitación (ORS siglas en ingles)

- Tarjetas de afrontamiento para transiciones saludables

- Traducción - Glosario Español

- Usando Estrategias Positivas para Proteger del Bullying a Su Hijo/a con Discapacidades

- Show all articles ( 20 ) Collapse Articles

-

Healthy Aging

- Articles coming soon

Reading Paystubs: Where’s the MAGI?

0 out of 5 stars

| 5 Stars | 0% | |

| 4 Stars | 0% | |

| 3 Stars | 0% | |

| 2 Stars | 0% | |

| 1 Stars | 0% |

27 Mar 1984, Washington, DC, USA — Washington: Clara Peller, star of Wendy’s commercial’s, asks her famous question, “Where’s the Beef,” during a press conference at a Washington Wendy’s. — Image by © Bettmann/CORBIS

Eligibility for Medicaid and advanced premium tax credits (APTCs) through HealthSourceRI (HSRI) is based on Modified Adjusted Gross Income (MAGI). But paystubs do not normally have a line for “MAGI.” This article describes how to find the MAGI on a paystub.

Please remember that Medicaid eligibility is based on current monthly MAGI, while APTC eligibility is based on a projection of annual MAGI for the relevant year.

For more information on MAGI for Medicaid, see this article.

For more information on MAGI for APTCs, see this article.

Also please keep in mind that many other types of income count towards MAGI. This article is only helpful at determining the portion of an applicant’s wages that count.

Finding MAGI on a paystub can be accomplished in three easy steps:

Step 1 – Identify Frequency of Pay

- Is the stub labelled as weekly? Bi-weekly? Monthly? If not, then look for the pay period.

- If no frequency or pay period is indicated, you may have to ask for more information.

The HSRI application allows you to indicated whether income is weekly, bi-weekly, or monthly. Then the computer does the math to calculate monthly and annual income.

But if you are not using the HSRI application:

- Convert weekly income to monthly income by multiplying by 4.33.

- Convert bi-weekly income to monthly income by multiplying by 2.165.

Step 2 – Is This Stub “Typical”?

- Does the paystub list any overtime? Bonuses? Any other items that lead you to believe that this is not a “typical” paystub?

- If so, you may need to seek more information, especially if projecting income for the purposes of APTC eligibility.

For the purposes of Medicaid, the most recent monthly income will govern. But for applicants with predictable fluctuating income (like a teacher with no summer pay), Medicaid must allow the applicant to ask that the fluctuations be taken into account, with eligibility based on average monthly income. For more information on fluctuating income and Medicaid eligibility, see EOHHS Rule 1307.06(03).

Step 3 – Find the MAGI

– Step 3a – Does the Stub List Federal Taxable Income?

Only federal taxable income counts in MAGI. If the stub lists something like “federal taxable income” or “federal taxable wages,” then this number will be the MAGI for the pay period in question.

– Step 3b – Does the Stub List Pre-Tax Deductions?

Some paystubs do not list federal taxable income, but they indicate that certain deductions are “pre-tax” or “excluded from federal taxable wages” (or something similar).

For these paystubs:

- Start with “gross income” or “gross wages”;

- Subtract the amounts indicated as pre-tax deductions.

- This will be the MAGI for the pay period in question.

– Step 3c – Is the Stub Unclear as to Taxable Income or Pre-Tax Deductions?

Many paystubs do not clearly list federal taxable income, or the deductions that are pre-tax, and so cannot be read using Steps 3a or 3b. For these paystubs:

- Start with “gross income” (which might be listed as “gross wages,” “gross earnings,” or something similar)

- You might be able to identify some deductions as pre-tax. Common pre-tax deductions include employee contributions to:

- health insurance premiums;

- 401(k)s and 403(b)s (and some other pension or retirement accounts);

- Dependent care accounts;

- Commuter expenses;

- flex spending accounts (FSAs) and health savings accounts (HSAs).

- If any of these items are clearly identified, then subtract them from the gross income.

- If the paystub is unclear, you may need more information.

- When in doubt, you can always use the gross income figure as MAGI. Especially for APTC recipients, a conservative estimate is often a good idea. If an applicant is near the Medicaid eligibility limit, then it will be more important to confirm his or her MAGI as precisely as possible.

Examples

Here are three examples. Explanations are provided below each paystub.

Step 1

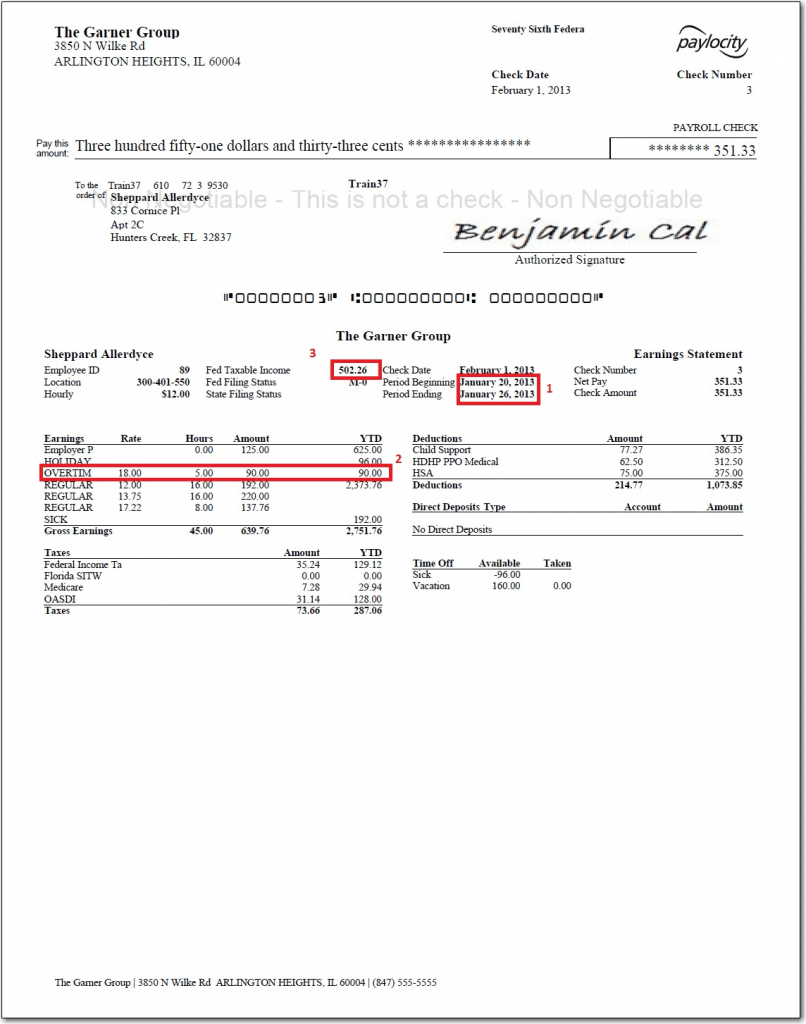

1 – The pay period on this check runs from January 20th to January 26th, making it a weekly check.

Step 2

2 – The check lists 5 hours of overtime ($90), and the Year-To-Date (YTD) column seems to indicate that this is the employee’s first overtime of the year. More information must be provided by the client about how often he expects to receive overtime pay. This information is especially important for projecting annual income for the purposes of APTC eligibility.

Step 3

3 – This paystub lists federal taxable wages, so finding the MAGI is easy. For the week represented by this paystub, the applicant’s MAGI from wages was $502.26.

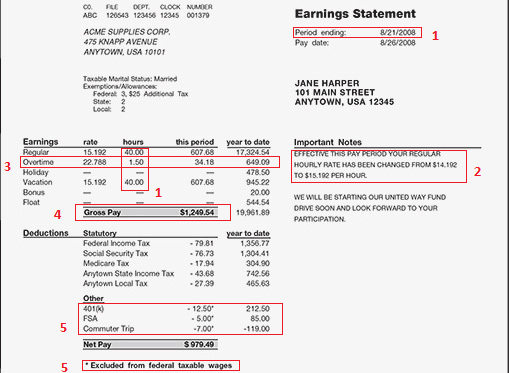

Step 1

1 – The pay period ended 8/21, but the stub does not clearly indicate a pay period. But since there are 80 hours of regular pay (or vacation pay) on this stub, it is highly likely that this is a bi-weekly paystub.

Step 2

2 – This paystub appears atypical for two reasons. First, the stub says that the employee’s hourly pay just increased. For Medicaid, the fact that his pay just increased is not so important (since Medicaid is based on current monthly income). But for APTCs, the change in pay is very important. When projecting his annual income for this year, you must account for this recent change.

3 – Overtime is the second reason this paystub may not be typical. This client should be asked if he normally works this amount of overtime. Judging by they year-to-date figures, this level of overtime may be normal.

Step 3b

This paystub does not clearly list federal taxable wages. But it does clearly show which deductions are excluded from federal taxable wages.

4 – The employee’s gross pay for the period was $1,249.54.

5 – Three deductions (401(k), FSA, and Commuter Trip) are clearly marked as being excluded from federal taxable wages.

Subtracting the pre-tax deductions (total $24.50) from the employee’s gross pay ($1,249.54) yields a MAGI for this pay period of $1,225.04.

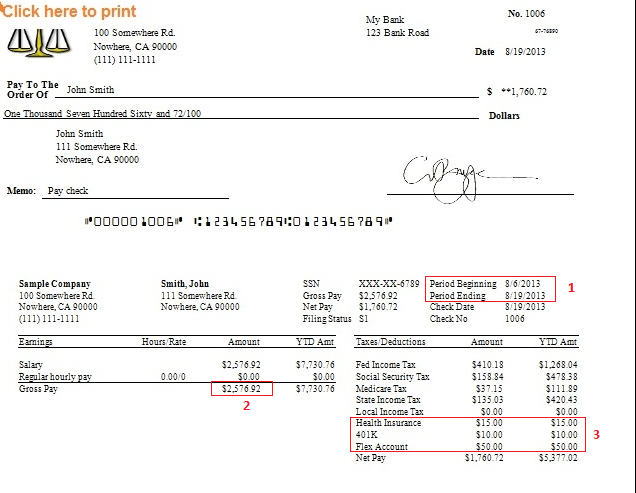

Step 1

1 – The pay period began 8/6 and ended 8/19, making this a bi-weekly check.

Step 2

There is nothing on this paycheck that makes it appear atpyical. The client should always be asked if this is a typical pay period.

Step 3c

This paystub does not indicate federal taxable wages. It also does not indicate which deductions are excluded from federal tax. We must therefore start with gross wages, then look for any known pre-tax deductions that can be subtracted out.

2 – The gross wages from this pay period were $2,576.92

3 – A few of the deductions are labelled as items that are generally excluded from federal taxable income. On this stub, those items are “Health Insurance,” “401K,” and “Flex Account.” For this pay period, those items total to $75.

Subtracting the pre-tax deductions ($75) from the gross income ($2,576.92) yields a MAGI from wages for this pay period of $2,501.92.

0 out of 5 stars

| 5 Stars | 0% | |

| 4 Stars | 0% | |

| 3 Stars | 0% | |

| 2 Stars | 0% | |

| 1 Stars | 0% |